The dreaded tax season is approaching fast for cryptocurrency traders and investors in the United States. Filing taxes is already a stressful process, and adding cryptocurrencies to the mix only serves to amplify that, especially with so much uncertainty on the matter.

This article is not meant to be financial advice, and you should still seek personalized tax advice if you are unsure about the proper actions to take. That said, hopefully the information and resources in this article will help point you in the right direction, significantly reducing the amount of time you need to spend researching on your own.

Cryptocurrency is Considered Property

The most relevant document when it comes to paying US federal taxes on your cryptocurrency transactions is Notice 2014-21. Unfortunately, this notice does not establish any clear and straightforward answers on exactly how to pay taxes. Rather, it attempts to fit cryptocurrencies into previously existing general tax principles.

In tax code, cryptocurrency is referred to as “convertible virtual currency.” The word “convertible” expresses the idea that virtual currencies, like Bitcoin, can be exchanged for legal tender like US dollars. As such, all virtual currency is treated like property for general tax purposes.

As a result of being considered property, all cryptocurrency exchanges are considered taxable events. This means that buying a cup of coffee with Bitcoin is a taxable event, as is exchanging Bitcoin for Ethereum or US dollars on an exchange.

However, it’s important to make the distinction between exchanges and transactions, because not all transactions are taxable events. The ones that aren’t taxable are those in which you send cryptocurrency from one wallet to another but you own both wallets. It’s the equivalent of moving money from your checking account to your savings account. No exchange takes place in those transactions, so they are not taxable.

Likewise, simply buying and holding cryptocurrency is not taxable. If you do not sell or exchange any cryptocurrencies in a given year, you do not owe any taxes on what you are holding.

Capital Gains and Losses

Being considered property, virtual currency is taxed very similarly to stocks and bonds. That means that you will pay capital gains or deduct capital losses on every taxable event.

There are four critical pieces of information you should know in order to pay or deduct the correct amount:

- The date that you first acquired the virtual currency

- The price at which you bought or otherwise acquired it, (including the transaction/deposit fee)

- The date that you sold or exchanged the virtual currency

- The price at which you sold or exchanged it (reduced by the transaction/withdrawal fee)

To take a quick example, suppose you bought I Decred for $5, plus paid a $1 exchange fee. Then you sold it for $50, and again paid a $1 exchange fee. In this case, your capital gain would be: (50-1) – (5+1) = (49 – 6) = $43. Even though the asset gained $45 in value between when you bought and sold it, you can deduct those fees from the gains.

Several exchange platforms offer some type of tax report based on your account activity. If you haven’t tracked all of your exchanges yourself, you’ll want to look for these reports. For future reference, though, it’s always best practice to do your own record keeping. Perhaps that’s easier said than done if you are an active trader, but it beats having the IRS come after you because the exchange you used went under or somehow screwed up your report. Better safe than sorry.

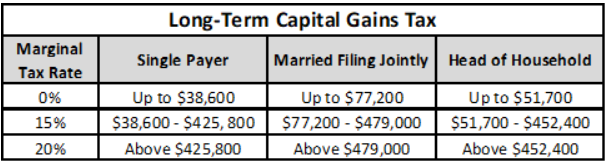

If you don’t have experience with capital gains and losses from other investments, information about how to calculate what you owe is easy to find. Capital gains are categorized as either long-term (usually greater than 1 year) or short-term. Short-term capital gains are taxed the same as income, so the rate will depend on which tax bracket you fall into. Long-term capital gains are taxed at a lower rate, also dependent on income as shown in the table below.

Capital gains or losses are simply the change in value from the time you buy an asset to the time you sell it. For example, if you buy 1 Bitcoin at $10,000 and sell it one week later for $11,000, you pay taxes on the $1,000 gain only.

If you lost money on an investment, it’s possible you can deduct that on your taxes. Losses can be categorized one of three ways: theft loss, casualty loss, or capital loss. If you were hacked, lost your hard drive, etc., you may be able to deduct those events as casualty or theft losses.

It should be noted that the maximum deduction for property losses in a single year is just $3,000. Additionally, you cannot calculate casualty losses based on the price of the asset at the time of the loss. Rather, the loss is calculated based on the price of the asset when you purchased or otherwise acquired it.

With the Tax Cuts and Jobs Act taking effect in 2018, deductions for casualty losses will no longer be possible for property assets that are not real estate. If you lost a hard drive with Bitcoin on it, this is the year to claim that loss on your tax report.

First-In-First-Out?

One other point to clarify is what to do with a specific virtual currency that you’ve bought on multiple occasions. For instance, suppose that you bought 0.1 Bitcoin every week for 10 weeks until you had 1 full BTC. Each time you bought, it was likely at a different price. Now, when you decide to sell 0.1 BTC, you have to calculate the gain or loss based on one of the 10 prices at which you bought.

This isn’t explicitly covered in Notice 2014-21 or elsewhere. However, the common practice with other property assets is first-in-first-out (FIFO). In other words, you would calculate your loss or gain for the 0.1 BTC you are selling based on the first 0.1 BTC that you bought.

Of course, there may be times when you can save money by doing something besides FIFO. There is nothing in the current legislation saying that you can’t do this, but it’s possible for future legislation to mandate FIFO retroactively. Should this happen and you calculated the tax owed for your crypto assets another way, you may have to go back and redo previous tax returns. However, for some people, it will likely be worth the risk to do last-in-first-out (LIFO) instead.

One way that FIFO can really come in handy is with long-term capital gains. For example, if you started buying Bitcoin consistently in 2015 and didn’t sell any of it until 2017, it would make sense to apply FIFO to your sales so that you pay long-term capital gains tax instead of short-term.

To the contrary, LIFO can really come in handy if you use a buying strategy like dollar cost averaging during a bull market. For example, imagine that you started regularly buying 1 ETH per month, starting on January 1, 2017. (Hopefully you don’t have to imagine!) Now suppose that you decided to take some profit for the first time in November when the price nearly passed $500.

In this case, LIFO would drastically reduce the amount of gains you have to pay taxes on for the proportion of your holdings that you sell. If you calculated the gains based on the price you bought on November 1, you’d owe taxes on about $160 in capital gains. If, instead, you used FIFO, you would owe on about $470 in capital gains.

With the incredible price volatility in cryptocurrency, your choice between LIFO and FIFO can make a big difference. The decision is ultimately up to you. If LIFO allows you to pay significantly less, it makes sense to go with it and take your chances with the IRS applying a FIFO standard retroactively.

Mining and Getting Paid in Cryptocurrency

If you mine cryptocurrencies or get paid with them, that is treated simply as income and taxed in the same way that it would be if it was a conventional income paid in US dollars. If you choose not to immediately sell whatever you’ve earned, you must still pay income tax on the original amount. Whatever loss or gain that you experience after that is taxed as described in the sections above.

Hard Forks and Airdrops

Hard forks and airdrops are two events in the cryptocurrency world that are ambiguous when it comes to taxes. For anybody who doesn’t know, an airdrop is an event in which a blockchain project distributes free tokens or coins to the community. This is a very successful marketing tactic and has been employed by well-known projects including Stellar Lumens and OmiseGo.

People who receive airdrops do so knowingly, so there’s no chance of playing the ignorance card in this case. As such, the safest way to treat airdrops is simply as you would income that gets paid in cryptocurrency. Whether you sell immediately or hold onto your free coins, you should plan to pay income taxes on the original amount you received.

As for hard forks, pleading ignorance is far more plausible. There have been more than a dozen Bitcoin hard forks since fall of 2017 alone. It would be hard for anybody to keep track of them all, let alone the average investor who might not even know what hard forks are. Taking that into account, treating hard forks as income and expecting all holders to account for all hard forks would be ridiculous.

What makes better sense is to simply assign a cost basis of zero to any forked coin that you receive. In other words, treat the forked coin as if you bought it the day of the fork. If it’s worth $30 the day that you received it and you sell at $40, the only taxable event is the sale with a capital gain of $10.

Other Helpful Resources

For an in-depth discussion of the topics touched on in this article, you can check out the January 23, 2018 episode of the Unchained podcast. It’s an approximately 1-hour long episode in which host Laura Shin talks to tax attorney, Tyson Cross, and CPA, Jason Tyra. They cover additional topics, including the risks of treating crypto-to-crypto exchanges as like-kind exchanges and deferring paying taxes on them.

Additionally, there are a few services that offer portfolio tracking and tax reports which can reduce some of your workload, especially if you have carried out trades on more than a handful of exchanges. The most popular and trusted of those services are https://bitcoin.tax/ and https://cointracking.info/, while https://koinly.io/ is an upcoming crypto tax calculator.

Final Takeaway

After the incredible bull market of 2017, it’s likely that capital gains taxes will be pretty steep for many of you reading this. However tempting it may be to just avoid this mess and keep your cryptocurrency portfolio off your tax filing, it’s certainly not wise to do so. We’ve already seen the IRS demand extensive records from Coinbase last year, and we know that new regulations are imminent.

Tax day is April 17 this year in the US. Stay ahead of the game and file your taxes with all virtual currency exchanges included to the best of your ability. Better a little headache now than steep penalties for tax evasion and a bigger headache somewhere down the line.